Integrated thinking and reporting (IR) is ‘the new kid on the block’, as highlighted at CIFPA’s recent International Seminar in Luxembourg.

So what is IR and does it have any relevance in the public sector? In an effort to answer these and other questions, CIPFA and the International Integrated Reporting Council (IIRC), sponsored by the World Bank, have published guidance, Focusing on Value Creation in the Public Sector (PDF, 761 KB).

The primary aim of the publication is to encourage dialogue and provide some foundation information that can be used by leaders of organisations who are considering adopting and/or implementing IR.

So why make the change from conventional financial reporting? Public sector spending is big business and accounts for almost one-third of GDP in most countries around the world. As big business, it is critical for financing infrastructure and providing good educational opportunities and effective health and welfare, but most importantly it helps to create the conditions for wealth creation now and well into the future. The drive for better scrutiny, constraints on time and resources and a working environment driven by constant change mean that we have reached a tipping point in the public sector, where financial information alone is no longer good enough to tell a story about how organisations create value – integrated reporting and thinking can help.

There are a number of public bodies worldwide that have adopted IR, but this number is too low when compared to advances made in the corporate sector – 1,000 corporate sector organisations around the world are now doing IR. Also, a piece of research commissioned by the IIRC highlights that out of 60 organisations surveyed, 72% of respondents said that IR had helped to improve decision-making.

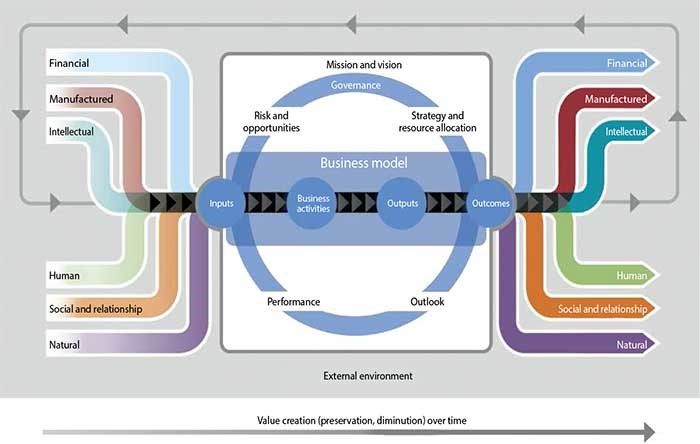

IR fosters a disciplined approach to decision-making that requires adopters to take a holistic view of how their resources and stakeholder relationships impact upon service delivery and most importantly the value they create. This is achieved with reference to the six capitals: human, financial, intellectual, social and relationships, manufactured and natural capital, as set out in the Value Creation Process shown in Figure 1.

Figure 1. The Value Creation Process (Adapted from the International IR Framework)

Through the lens of the six capitals of IR, public sector entities can transform the way they think about organisational strategy, business processes and governance. IR can help guide public bodies in their day-to-day reasoning, decision-making and actions to consider the resulting impact across different time horizons; not limited to the traditional myopic short or medium timeframe.

IR explains how sustainable outcomes will be delivered to meet the requirements of different stakeholders over time. Building on the tenets of integrated thinking, it extracts and consolidates the substance of what matters, ensuring that there is integrity in what is reported and alignment of reporting requirements against associated risks, opportunities and performance. At the heart of IR are some fundamental principles:

- Strategic focus and future orientation – insight into the organisation’s strategy and how it relates to the organisation’s ability to create value in the short, medium and long-term.

- Connectivity of information – a holistic picture of the combination, interrelation and dependencies between the factors that affect the organisation’s ability to create value over time.

- Stakeholder relationships – insight into the nature and quality of the organisation’s relationships with its key stakeholders, including how and to what extent the organisation understands, takes into account and responds to their legitimate needs and interests.

- Materiality – information about matters that substantively affect the organisation’s ability to create value over the short, medium and long term.

- Conciseness.

- Reliability and completeness – disclosure of all material matters, both positive and negative, in a balanced way.

There is little doubt that the IR framework has a lot to offer public bodies. CIPFA in partnership with the IIRC recognises this, and for the last three years has been running a Public Sector Pioneer Network (PSPN) that is assisting public sector organisations in adopting integrating thinking and reporting. Its current membership is over 200 participants in over 122 countries.

Next year is going to be an exciting year for the Pioneer Network as there are a number of initiatives taking place, not least CIPFA will be developing an application note for IR in the public sector to help public bodies implement IR.

Discover more